Why can’t every country pay for disasters like Jamaica?

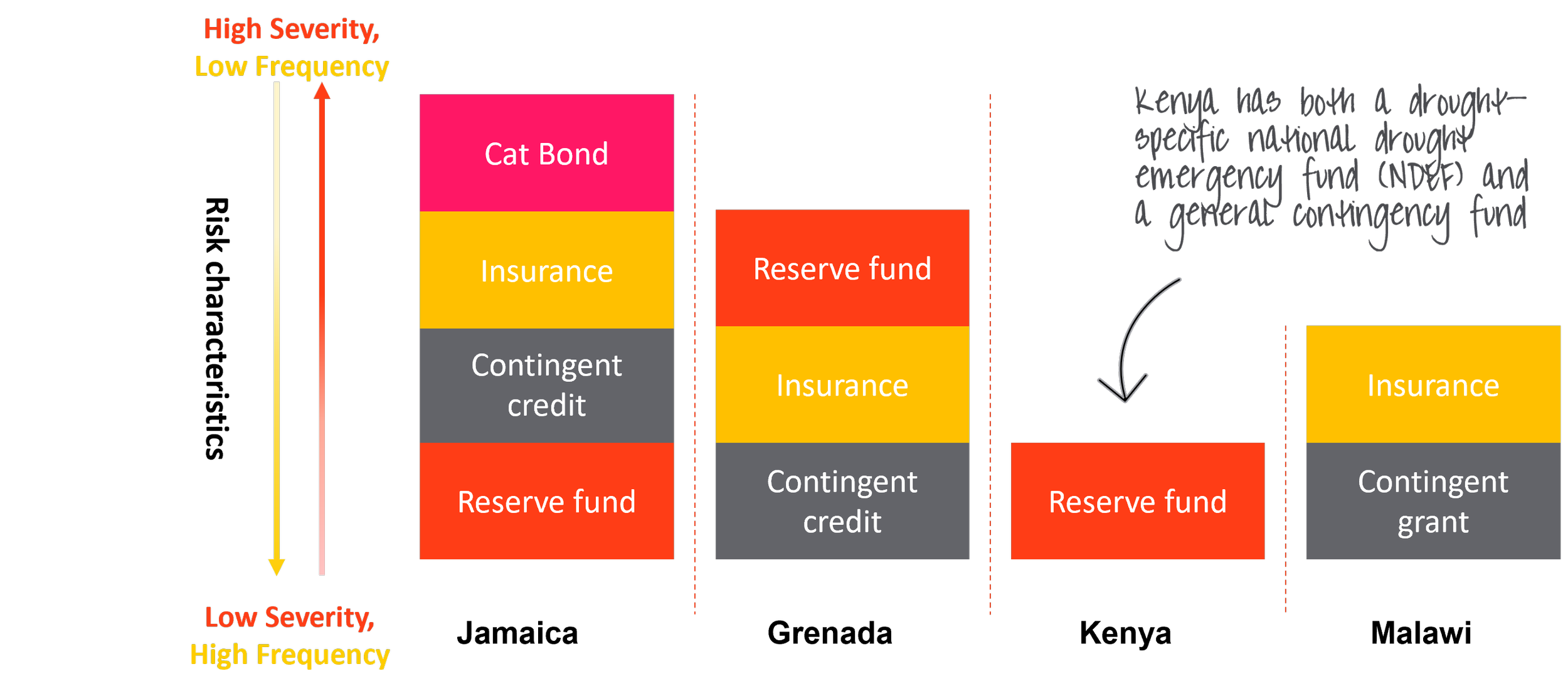

Risk layering in disaster financing has helped countries improve financial preparedness for natural hazards. It is often presented as a neat technical exercise: countries should retain risk for frequent, low-severity events through relatively inexpensive budget reserves and contingent credit or grants, while transferring rare, catastrophic risks through more costly insurance and catastrophe bonds. Yet many countries don't follow the model. For good reason.

Each country faces distinct objectives, disaster risks, funding options, and fiscal constraints when designing its financing strategies and choosing disaster risk financing instruments. Once a crisis occurs, the calculus shifts again. Pre-arranged instruments trigger (or fail to), emergency fundraising materialises unevenly, and government expenditure priorities evolve, all shaping how pre-arranged funds are deployed. These real-world complexities mean policymakers frequently deviate from traditional risk-layering models. A comparative look at four countries shows that deviations from the risk-layering model are not failures of design.

Jamaica: The textbook approach

Jamaica provides one of the clearest real-world demonstrations of the traditional layered model of financial preparedness. Over more than a decade, the government built a “financial fortress” of pre-arranged disaster risk financing. This includes budget reserves, contingent credit from multilateral development banks and the IMF, parametric insurance through the Caribbean Catastrophe Risk Insurance Facility (CCRIF), and a sovereign catastrophe bond.

When Hurricane Beryl struck as a Category 4 storm in 2024, Jamaica drew on domestic reserves and had access to external contingent credit and insurance payouts, but its catastrophe bond did not trigger. When Hurricane Melissa hit as a Category 5 hurricane in 2025, the country’s catastrophe bond did trigger. It illustrated the intended function of top-layer risk transfer instruments: protecting public finances against rare, extreme losses that would otherwise overwhelm national buffers. At the time of writing, Jamaica appears to have utilised domestic reserves, contingent credit and insurance payouts, including catastrophe bond payouts, in its response to Hurricane Melissa.

The Jamaican case shows the risk layering model working broadly as designed. But it is not the only approach to financial preparedness. Other countries have adopted materially different but no less rational strategies. Three factors explain why: regulatory frameworks, external relationships and fiscal incentives.

Grenada: Regulatory frameworks

When Hurricane Beryl struck, unlike Jamaica, Grenada drew down its US $20 million contingent funding line with the World Bank (known as Catastrophe Deferred Drawdown Options, or Cat DDOs), and received a US $44 million payout from CCRIF while leaving its domestic contingency fund (of similar size) untouched. This was by design: Grenada’s National Transformation Fund regulation dictates that the country’s national contingency fund “is available only to the extent that [disaster] costs exceed payments from alternate sources, including contingent lines of credit and catastrophic insurance”. In other words, the contingency fund is not intended to absorb disaster losses per se, but rather to protect against the risk that adequate external financing fails to materialise.

This also introduces an interesting additional consideration regarding when a country like Grenada might draw down its contingent funding line with the World Bank. Grenada is required by regulation to draw down external contingent funding, given that it is designed to serve as the first source of pre-arranged financing. This illustrates additional considerations for how Cat DDOs are actually used. In theory, these instruments are held in reserve for relatively rare disasters. In practice, for a variety of reasons, countries draw on them much sooner and often within 18 months of activation.

Kenya: External relationships

Kenya illustrates another set of design choices. Drought costs Kenya an estimated 8.0% of GDP every five years, compared to 5.5% of GDP every seven years for flooding. Kenya’s National Drought Emergency Fund, or NDEF, was established to manage this relatively high exposure to drought. Yet drought attracts 92% of disaster financing in Kenya, compared to less than 3% for flooding between 2016 and 2021.

Kenya’s focus on drought seems, in part, to have been informed by development partners (such as the UK government and World Bank). Kenya’s NDEF was operationalised after almost a decade of “sustained investment and engagement” by the country’s partners, including through hunger-specific programming. The stakes of risk-layering are not abstract; in March 2026, at least 42 people were killed as flash floods swept through Nairobi and several other Kenyan counties. This follows severe flooding between October 2023 and May 2024, which killed over 200 people and displaced over 200,000 people across the country.

While Kenya has historically had a risk-layered strategy that included insurance and contingent credit, these instruments were last available in 2016 and 2022, respectively. In the current disaster risk financing strategy development process, which the Centre is supporting, Kenyan authorities are exploring the potential to broaden the range of hazards covered, with the aim of including populations affected by other hazards such as floods and landslides. [1]

Malawi: Fiscal incentives and constraints

Malawi has yet to operationalise its domestic contingency funds, the first line of defence in a traditional risk-layering strategy. Instead, over the past decade, Malawi has arranged and triggered contingent grants with the World Bank and parametric insurance with a regional risk pool, the African Risk Capacity, or ‘ARC’, Group. The World Bank contingent instruments provide pre-arranged access to funding that can be drawn down once a disaster is declared.

Malawi has highly advantageous terms with the World Bank, and donors subsidise its parametric insurance premiums. In both cases, this assistance was from dedicated disaster risk financing windows, meaning Malawi faced limited opportunity costs to using grants in this way. Conversely, domestic contingency funds may have to be capitalised from scarce general budgetary resources that could be used for other public expenditure priorities. For IDA-eligible countries (like Malawi), the World Bank’s concessional lending structure means that every dollar held in reserve through a Cat DDO unlocks three additional dollars in contingent financing. Triggering early to access this additional funding is therefore rational. [2]

The diagram below shows how each country’s approach has differed. Each has tailored its strategy, which, in turn, reflects risk exposure, available instruments and fiscal incentives.

Beyond ‘best practice’

The examples highlight the role of international assistance and development partners in shaping countries’ approach to disaster risk. Donor programmes are influenced by the availability of risk modelling and feasibility for specific perils and can favour specific instruments, shaping domestic decisions. This raises an important test for policymakers and partners alike: if disaster risk finance assistance were transferred directly into government budgets, would it be allocated in the same way? If not, are donors confident that their preferred financing structures outperform locally determined priorities?

Risk layering, in short, is not simply a technical exercise in financial engineering. It is a politically mediated process of matching scarce resources to uncertain shocks – shaped by context, influenced by external actors and responsive to incentives. That is where any honest framework for improving disaster financing must start.

[1] Kenya also hosts programme-level insurance mechanisms, such as the World Bank (and ZEP-RE)'s DRIVE programme, which operate at the humanitarian rather than sovereign level. Further downstream, the government has also taken steps to transfer disaster risk from private actors in the agriculture sector to its own balance sheet, reducing vulnerability in the sector by increasing sovereign contingent liabilities.

[2] It is also worth noting that the World Bank's REPAIR programme provides a bundled risk-layering stack for Malawi that begins outside the government's own financing architecture but is triggered by government and deployed through national structures, illustrating how the line between sovereign and external disaster finance can blur in practice.

Emerging Lessons On Pre-Agreed Financing For Shock-Responsive Social Protection In Jamaica

Article Glossary

More Insights

If local actors are meant to hold more decision-making power over disaster finance, the case is stronger when the research making it was designed to shift power too.

Read more

Launching: Counter Crisis Season 3

The brand new season of Counter Crisis is released today.

Read more

Climate risk finance works better when more voices are in the room. Early evidence from Pakistan, Costa Rica and The Gambia shows how that idea holds up and where it still falls short.

Read more